Searching for a solution: What matters to Financial Services Firms in the Market for New Software?

Executive Summary

Legacy’s still the biggest blocker for digital

Outdated infrastructure is still getting in the way of successful digital transformation.

Covid has shown up the cracks in internal processes

The pandemic has revealed gaps in FS firms’ process optimization efforts.

Buy trumps build

More FS firms want to buy software solutions from the experts than go it alone and build internally.

Implementation has to be easy

FS firms in the market for new software solutions put ease of implementation top of their list.

Compliance is the key

Having all the right regulatory boxes ticked is the most important factor in successful solution integration.

Talent is top of the agenda in the near term

FS firms are focusing their energies on attracting the right people to their organisations over the next 12-18 months.

Private Cloud and On-Premises are preferred over SaaS

SaaS options come last in order of preference for FS players on the hunt for new solutions.

Word of mouth is crucial for trust

Peer recommendations comes out on top as the most important factor when deciding if a new solution provider is trustworthy.

Methodology

In Q1 of 2021, FinTech Connect surveyed 100 financial services leaders from across Europe to find out more about their digital transformation challenges, the impact the global pandemic has had on their businesses, and their preferred approach to procuring and integrating software solutions. The results were compiled and anonymised by FinTech Connect and are presented here with analysis and commentary from Aurum.

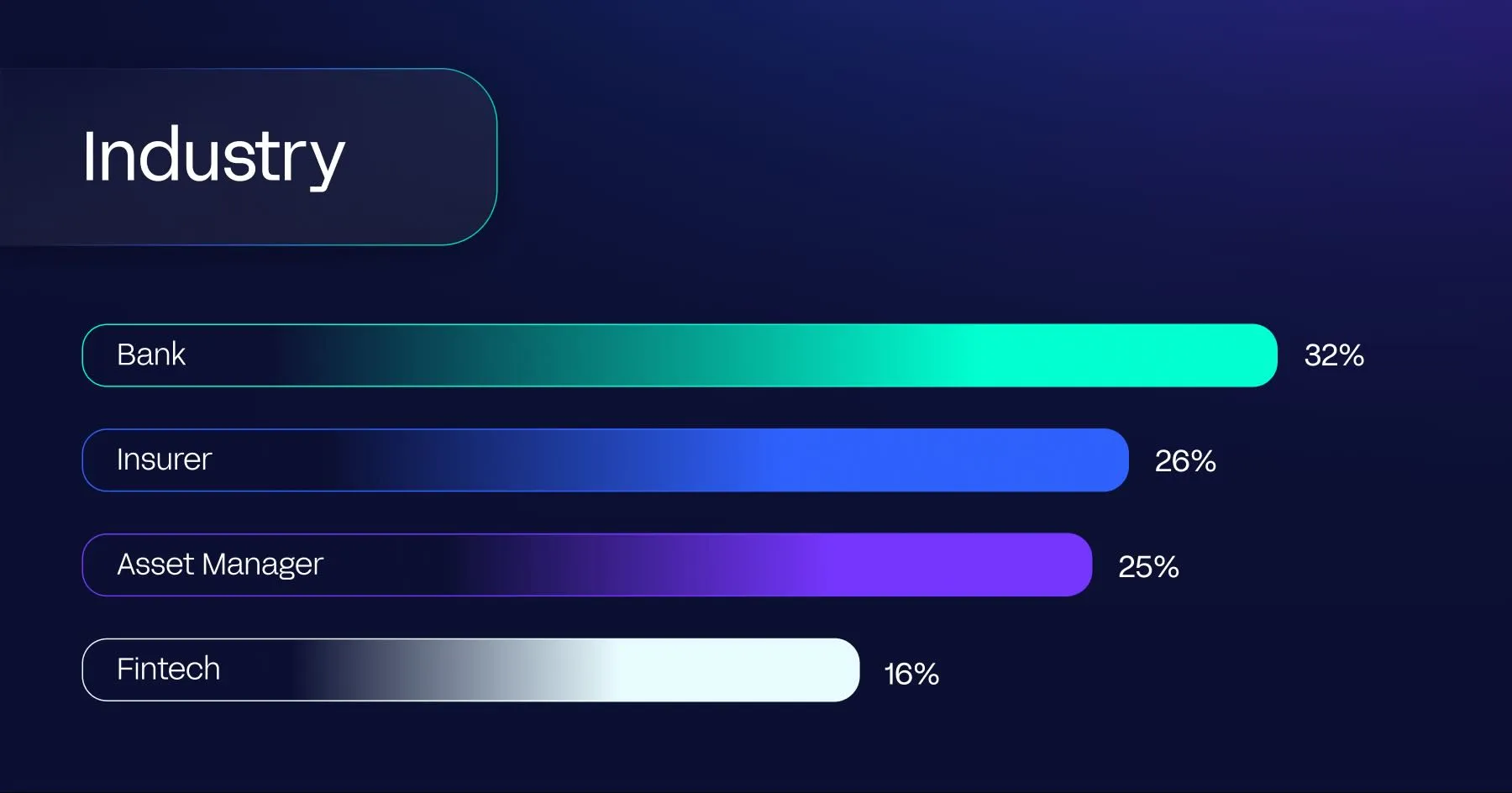

The majority of respondents worked in the banking sector, with participation also amongst those in insurance, asset management and fintech:

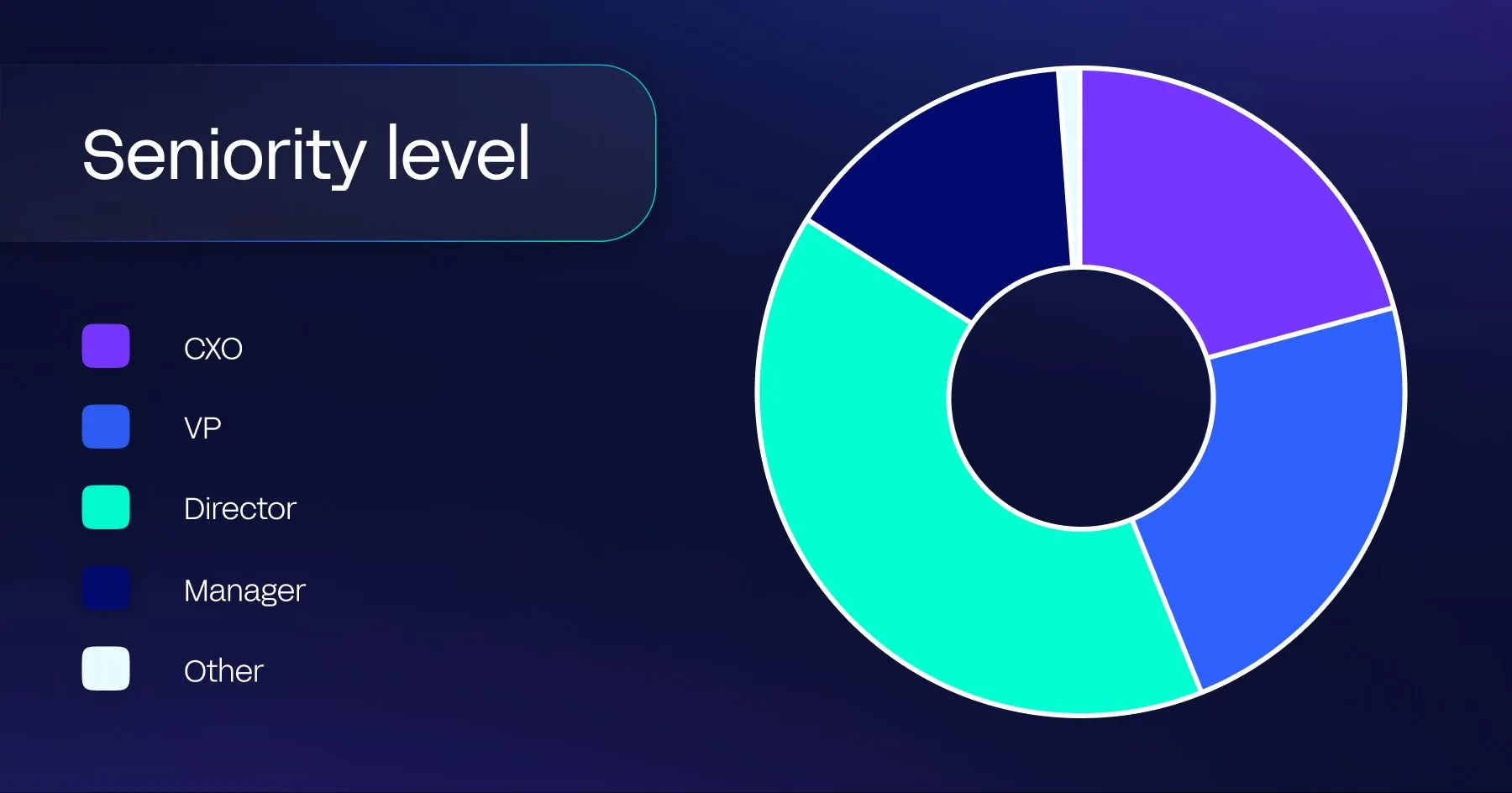

All respondents were senior, holding positions such as CXO, VP, Director and Manager:

Respondents worked for businesses of varying sizes but most were employed by those with a headcount of over 1,000:

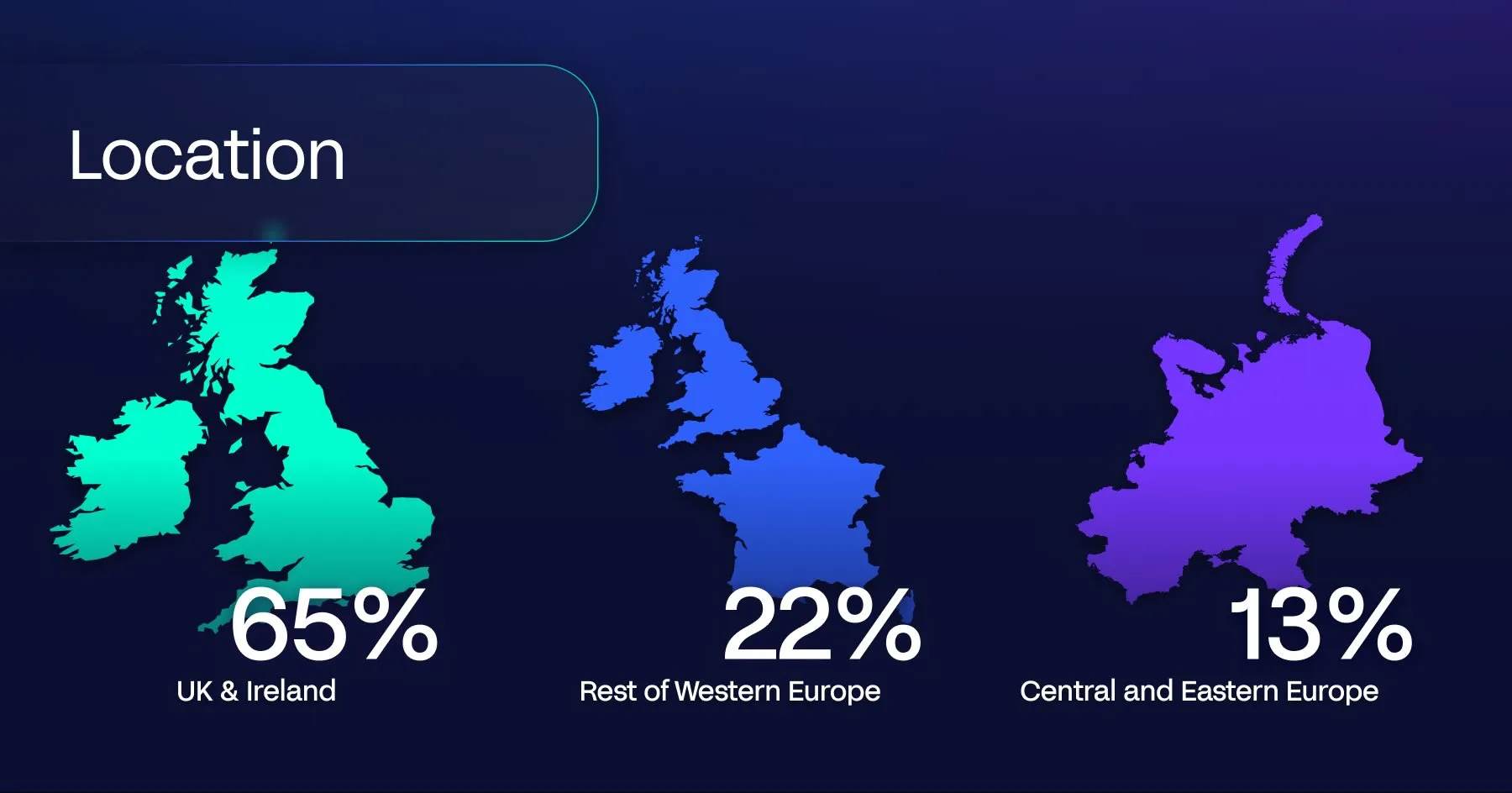

The survey was conducted across Europe, with most input sourced from the UK and Ireland:

Digital blockers

FS firms have been on a mission to get fit for the digital age for years now, and the behaviour changes forced by the ongoing global pandemic have only served to sharpen industry leaders’ focus on meeting digital demands.

While some FS firms have opted for greenfield plays and the promises of a clean slate, many have taken a more gradual, piecemeal approach to digital reinvention.

This likely accounts for our participants’ chief challenge being integrating with legacy tech. In some ways, it’s unsurprising: legacy is the problem that simply won’t go away. It’s often cited by FS executives as the number one obstacle to digital progress, and it continues to consume the lion’s share of IT spending for many institutions. Inflexible and outdated, legacy still has the potential to slam the brakes on even the most well-managed digital transformation projects.

Our research also suggests that understanding what can and can’t be achieved by the implementation of new technologies is crucial for creating real, sustainable digital change. Whether it’s recognizing that some celebrated innovations are really still solutions in search of a problem, or part of encouraging a company-wide culture shift to embrace a digital-first mentality, clarity about what’s actually achievable is essential. This could explain why our participants reported that misconceptions of new tech represent the second biggest challenge to becoming truly digital.

It stands to reason, then, that lack of proof in tangible end results and an immediate focus on core business functions should be ranked as less important. Proof of the benefits of digitalization abound, from operational efficiencies to improved customer experience, and there are few businesses today that can put off the shift to digital and continue to narrowly focus on core areas of the business.

The COVID effect

When it hit, COVID-19 unleashed a wave of speculation across the fintech ecosystem: who had their house in order? Who wouldn’t survive? Will investment dry up? What will the future look like? And, for transnational corporates and start-ups alike, much has been made of the effect of covid-19 on business performance. So, rather than add to the conjecture, we asked our survey panel to order these effects of the pandemic in terms of their impact on their businesses.

For our survey respondents, the top-ranked effect of the pandemic is that it has exposed gaps in process optimisation. Although the proportion of ‘in-person only’ customers has been shrinking for years and, relatedly, the majority continue to switch to ‘digital-only’/ ‘hybrid’ approaches to consuming financial services, the first national lockdowns pulled the rug on players big and small. As demand for digital services rocketed, it showed up the cracks, bottlenecks and pain points of everyday operations.

At the same time, the upheavals caused by the pandemic have accelerated innovation that otherwise would still be in R&D. Of course, this is in large part a development borne of necessity, with FS players rising to the demands of our new ‘digital moment’. But many have consciously resisted the urge to deprioritize their innovation agendas too: rather than press pause on innovative digital projects, some FS firms have seized the opportunity to ramp up their development. It may be that FS players of a certain stripe learned the lessons of the last great shock to the sector, when financial hardship meant digital change ground to a halt, only for them to emerge on the other side to find trailblazing fintechs eyeing up their market share.

Less important has been a focus on cash flow, and this could be due to the pandemic affecting firms differently: FS players heavily reliant on strong consumer spending may have seen coffers begin to run dry, but others haven’t fared so poorly. Understandably, outsourcing due to lack of internal resources registered the least impact for our participants, as furloughs and redundancies have been the more common workforce trends.

Buy vs. Build

When it comes to procuring software solutions, the majority of our respondents prefer to buy from the experts. The case for partnering with a solution provider on digital innovation initiatives has been made time and again, and the advantages are now well known: firms that partner avoid substantial development costs, don’t have to worry about ongoing maintenance and free up internal resources while accessing a tried and tested solution to their specific business challenges.

Still, a sizable proportion of our participants said their preference is to build software platforms and solutions in-house. Yet many FS firms have struggled to deliver at-scale impact using internal expertise and resources – the barriers, from difficulty attracting the right talent and the constraints imposed by legacy infrastructure, have been too great.

This has led the majority of established FS players to the conclusion that purchasing solutions is often the fastest route to delivering returns, recognizing that once they have defined clear goals and a strategy to achieve them, sourcing new capabilities externally offers the quickest way to create value for both the business and its customers.

Choosing a solution

Before the pandemic, most FS firms were behind where they’d wanted to be in terms of digital transformation. Yet now many are ramping up their digital efforts to meet the demands of the ‘new normal’. While this commitment is undoubtedly welcome, legacy can’t be cast off so quickly. This explains why the biggest factor when assessing a new solution is its ease of implementation.

Simply put, FS firms need to the ability to move at speed: business agility is critical to responding to shifting demands and seizing new market opportunities. Solutions that are easy to implement, that offer access to new capabilities with minimal effort, are key to giving FS firms the agility they need to cut time-to-market and start seeing value sooner.

Second in order of importance was bottom line financial benefit. Of course, digital transformation has allowed FS firms to make great progress on cost reductions: innovation in operations has achieved the kind of efficiency gains that have enabled FS players to provide better services while reducing spending, boosting profitability and freeing up resources for further digitalization initiatives.

But there is pressure now to show that FS firms of all sizes can use new tech solutions to boost profitability, whether by taking market share from competitors, launching new products or tapping into new revenue streams. This pressure will be more keenly felt in the context of the financial constraints imposed by the pandemic, so it is little surprise that financial effects rank so highly for our participants.

Trust and relationships with a provider registered third. This is a topic returned to in more detail in subsequent sections, but the importance of personal factors in our respondents’ decision making is clear. It’s interesting that being seen at the vanguard of tech is afforded less importance, suggesting that ‘innovation theatre’ may finally have had its day, while cost taking fifth place points to our participants’ belief that value for money is what matters most.

Making integration work

While choosing a solution provider can be a long and difficult process, the work of integrating with in-house systems brings its own challenges. So, we put it to our respondents: what’s the key driver to making a success of solution integration?

For our participants, by far the most important driver in a successful solution integration is strong compliance and regulatory measures, and this is understandable. With regulators dangling the threat of hefty fines for failings, and with customer trust in part dependent on robust measures being in place, FS firms have to take every step to ensure that they are meeting requirements during and after solution integration.

A proven track record of integrations with similar companies was tied with having modular components in the technology as the next most important factor in determining whether an integration is successful or not.

When choosing a provider, there is undoubtedly value in opting for a partner who has had experience of working with similar firms, as they’ll be attuned to the possible pitfalls during integration and will have had the opportunity to devise fixes. Similarly, modular components allow for greater flexibility in approach, giving FS players the opportunity to customize a solution in order to smooth the process of implementation.

It’s telling that guidance and tech support from the solution provider is ranked in last place. On-hand assistance is of course valuable to FS clients, but it has over time come to be regarded as a minimum requirement.

Near-term priorities

Taking the world by surprise, the onset of the global pandemic ground strategic developments to a halt. As FS firms knuckled down to maintaining something remotely resembling ‘business as usual’, future plans took a backseat. Now, one year on from the onset of covid, FS players can afford to be more forward looking, so we asked our participants to rank their business priorities over the coming 12-18 months.

The results indicate that the number one priority for FS firms as the world makes a slow return to normality is to build their team and develop talent. For years, whole economies have been suffering from a discernable ‘digital skills gap’, and the FS sector hasn’t been insulated from these shortages. By demonstrating the need for faster and more comprehensive digitalization, recent global events have also pointed to the urgency with which firms need to develop the teams with the right expertise and tools to drive real digital change.

In second position in our ranking of business priorities over the near term is optimising internal systems. With widespread remote working, the shuttering of branches and offices, and a sharp increase in the demand for digital services combining to test the robustness and, in some cases, the viability of operating models across the sector, this focus is perhaps unsurprising. Covid has revealed the cracks in how some firms do business and senior leaders will be eager to fix them, both in anticipation of future shocks and as a means of gaining on more digitally savvy rivals.

It’s noteworthy that the lower-ranked priorities relate to maintaining and growing the customer base. Rather than being untroubled by customer acquisition or servicing key clients, it could be the case that respondents feel that the present moment is the right time for their businesses to get their houses in order – to make urgent repairs while getting the right talent and tools in place, ready to compete on a stronger footing in the post-pandemic future.

Cloud, on-premise or SaaS?

Cloud-based but privately hosted solutions were the clear favourite among our survey participants. The ability to harness the benefits of cloud technologies while retaining control over the infrastructure is without a doubt compelling for many FS firms. And then there’s the issue of cost. For years, IT spend has been burning budgets, often solely for the task of keeping the lights on. In the context of financial constraints and an uncertain macroeconomic environment, cloud-based, privately hosted solutions offer reduced costs.

There are, of course, other significant advantages, ranging from more control over data to the greater likelihood of ensuring business continuity should a vendor have an outage. Finally, operating in a heavily regulated industry means FS firms are attracted to the increased security and privacy of privately hosted solutions, as sensitive data is stored on servers that only the firm in question has access to.

That on-premise solutions came second shows that, for FS firms with the balance sheet to afford the upfront investment and ongoing maintenance, the ability to retain greater control over the development of their capabilities remains important.

Interestingly, SaaS solutions came in last position for the FS firms surveyed, suggesting that security concerns around the management of sensitive data, the potential for outages arising from connectivity issues, and the lack of control over the development of the solution are big factors in the decision-making process and, on balance, make SaaS the least attractive option.

Building trust

Who can you trust to get the job done, to deliver on time and on budget? For FS firms scoping new digital projects, it’s one of the most pressing questions on the agenda. Ultimately, FS players put their reputations on the line when they roll out, say, a new offering to their customers, so having faith in the abilities of a solution provider to deliver is crucial. But how are potential partners judged? We asked our participants to tell us the most important factors that go into deciding if a new provider is trustworthy or not.

Word of mouth was by far the strongest factor, as peer recommendation took the top spot among our respondents. The fact that having a teammate or counterpart in another organization give a provider the thumbs up has the greatest influence on trustworthiness shows that vendors should double down on customer loyalty. Offering exceptional service and loyalty incentives can turn your customer base into your biggest promoters, helping to win new business.

A relatively close second in determining trustworthiness was a past working relationship, and this makes sense. If, from your point of view, a solution provider has been tried and tested, and has even delivered results to a previous organization, you’re going to carry that positive relationship forward. Maintaining visibility in the media and on social media was also reported to be a trust builder. Being seen as an active participant in the fintech ecosystem, engaging in debates and responding to trends, naturally builds credibility and confidence.

Of lesser importance to our respondents when judging providers was whether they had seen them speak at a conference or as part of a webinar or produced pieces of content marketing. This suggests, overall, that the personal trumps the promotional when it comes to building a reputation as a trusted provider.

How can Aurum help?

Stop struggling with data and legacy systems

Because we are data agnostic, our reconciliation platform can integrate with any system and data source. This means you can import data from any sources, including the legacy systems that simply won’t go away.

Trust our clients’ success

Our proven track record of successful integrations speaks louder than our words. Over the past 17 years we successfully implemented Aurum across

Financial Services Firms: banks, cross border payments, PSPs, FinTechs, Asset Management Firms, and several others.

Choose a solution built for you

Our highly flexible software allows us to tailor solutions in partnership with you that can be smoothly implemented, tackling all your business requirements.

Stay compliant forever

We worry about evolving regulations, so you don’t have to. Our strong compliance and regulatory measures are here to make sure you meet all

regulator’s requirements during and after our solutions are integrated.

Cloud-based privately hosted gives you the best of both worlds

By implementing our system in a private cloud, you get the flexibility of having complete control over your clients’ data and infrastructure. Aurum’s software was designed to give our clients a choice: traditional on-premises, or private cloud.

Ross McGee is a marketing manager at Aurum Solutions who deep dives into financial processes, technology, and best practices to share insights that help finance professionals of all levels maximise their potential.