UK Business Confidence Hits Record Low as Financial Challenges Force Closures Across Key Sectors

The UK economy has recently faced a series of challenges, with many businesses suffering from mounting financial pressures. Rising taxes, increasing national wages, and escalating day-to-day expenses, from electricity to fuel, mean that 2026 could be another difficult year for companies across the country.

Although GDP saw a slight increase, with real GDP growing by 0.1% in Q4 2025, unemployment still rose to 5% by the end of the year. Coupled with growing political uncertainty, these conditions are forcing businesses to operate more cautiously, reassess long-term strategies, and adapt quickly to shifting market realities.

Recent research from the FSB highlights the scale of the challenge: more than a third (35%) of small businesses expect to close or contract over the coming year. The picture is even starker in certain industries, rising to 41% in wholesale and retail and 45% in accommodation and food services.

Off the back of this, fintech company Aurum Solutions has analysed which parts of the UK are seeing the highest levels of business closures and which sectors are being hit the hardest, revealing where targeted investment may be needed.

The biggest challenges for businesses

While the government remains positive about the increase in economic growth, companies aren’t sharing the same view. UK business confidence in 2026 is low, with the Economic Confidence Index falling to a record low of -76 in March, driven by rising labour costs, tax pressures, and geopolitical uncertainty

Key challenges for businesses this year

Increasing Costs

The start of a new financial year brings rising costs across many sectors, particularly in everyday essentials. From April, the effects of inflation and the increase in the National Living Wage began to take hold. According to the FSB, a small employer with nine staff on the National Living Wage will have seen its annual employment costs rise by £25,850 between January 2025 and April 2026.

Business rates are also increasing for many organisations in England and Wales from 1 April 2026, following a national revaluation based on April 2024 property values. It is reported that business rates will rise by 10%, taking the total bill to more than £37 billion.

When combined with additional tax rises and further increases in energy prices, it is no surprise that many businesses are feeling less confident about their growth prospects for the year ahead.

Trade and political instability

Political uncertainty throughout the start of 2026 has created a volatile market, increasing risks for businesses, leading to potentially slower growth. In certain industries, supply chain risks around imported goods could cause logistical issues, resulting in unfulfilled orders. This, combined with rising fuel costs for transportation, warehousing and logistics businesses, can add to further business turmoil. If uncertainty continues, businesses may face significant challenges for the rest of the year, while declining investor confidence could further reduce funding in struggling markets.

AI integration

More than 90% of businesses now use at least one AI tool, and this will likely only increase as businesses adopt new technologies to enhance digital growth. However, investment in AI strategies comes at a cost for businesses, small and large. Making sure you stay ahead of your competitors in AI adoption, yet managing your funds in a market you may not have thought about investing in, could be an issue for many sectors. While adopting new technology can bring efficiencies, uncertainty about AI's impact on roles is still a cause for concern across many sectors, and how companies deal with this narrative could affect their employees.

With these being just some of the challenges businesses have faced at the start of 2026, it is no surprise that many feel forced to close their doors. A lack of investment, increasing financial strain, and rising competition are placing significant pressure on organisations across the UK. These factors have contributed to higher closure rates in certain sectors.

Where in the UK is suffering the most from business closures?

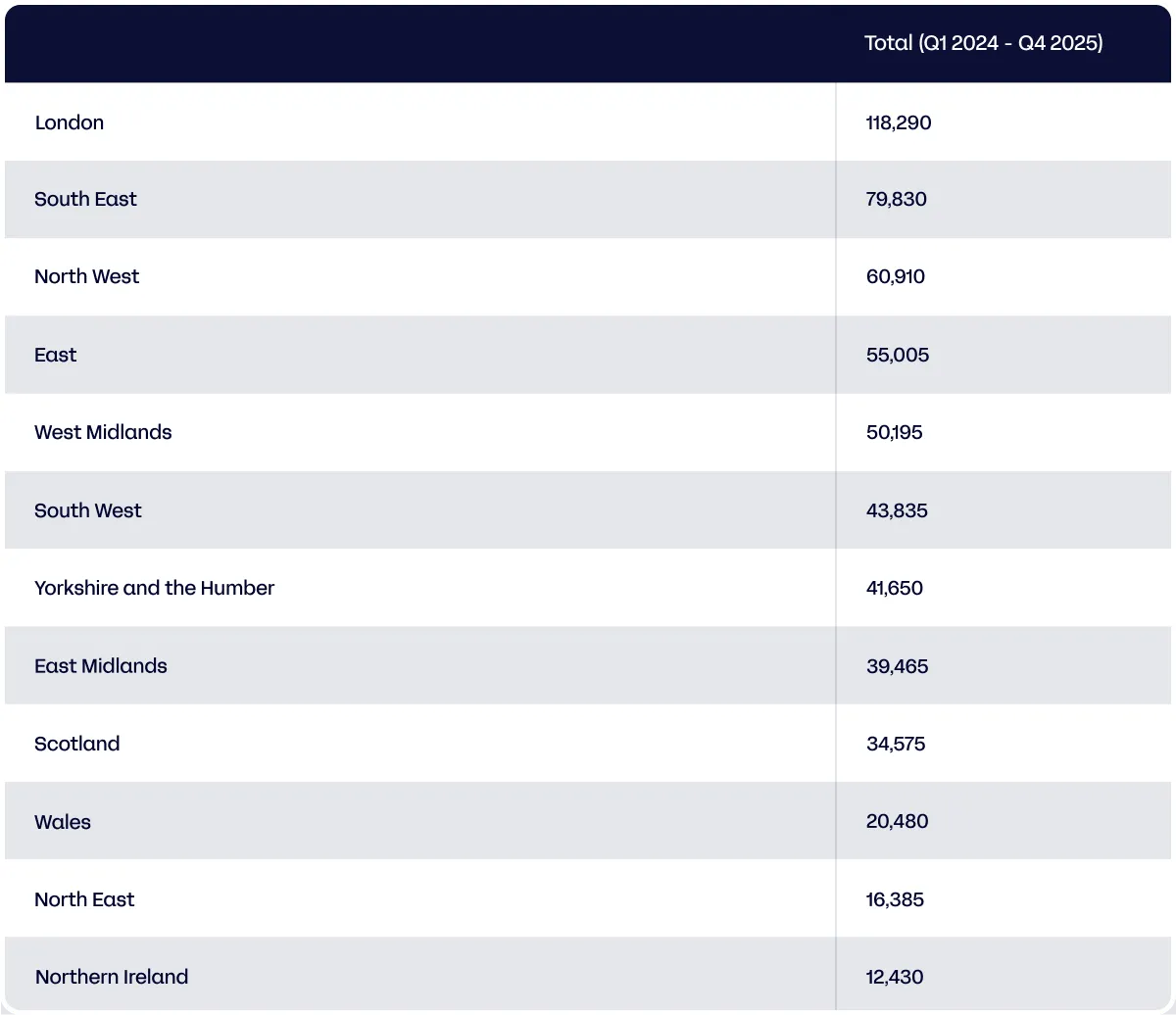

It’s been revealed that 581,060 businesses ceased to trade in the last year, from Q1 in 2024 to Q4 in 2025. Referred to as a business death, this means the closure, dissolution, or cessation of trade of a business entity, effectively marking the end of its operations. The business death rate was 9.8% across the UK, the lowest since 2016.

Analysis from ONS revealed that London (118,290) experienced the highest number of business closures last year. With the capital home to the largest population and key business hubs, it is unsurprising that the number of closures there was so high.

The South East, which ranked second on the list (79,830), also saw significant business closures. The region is an attractive location for businesses, close to London but with lower costs. However, while classic commuter cities may benefit from proximity to the capital, the advantages of being just outside London may be outweighed by intense competition. Areas such as Kent (13,090) and Surrey (11,985) ranked highly for business closures across the UK and topped those in the South East; accounting for 31% of all business closures in the region.

The North West ranked third (60,910), which may come as a surprise. The region boasts a strong business hub, particularly in media, centred around cities such as Liverpool and Manchester. However, growing competition in these sectors may have contributed to the higher closure rate. Greater Manchester saw over 26,000 business deaths across 2024-2025, generating 43% of all the North West business closures for the year.

The regions suffering the most from business closures

Northern Ireland saw the smallest number of business closures throughout the year, with 12,430 closures. This was followed by the North East region with 16,385.

While typically these regions aren’t synonymous with major business hubs, they often specialise in niche sectors such as manufacturing, which may offer greater resilience during economic downturns. However, even these modest losses may still indicate underlying challenges in these areas and a need for further investment.

On average, 71,000 businesses close every quarter.

Taking the average of each region across the different quarters, around 71,000 businesses could be set to close over the next quarter, it has been revealed.

On average, 71,631 businesses closed over the past year. Quarter one in both 2024 and 2025 saw the highest number of business closures, with the start of the new financial year proving particularly challenging for some businesses and ultimately leading to their closure.

Quarter three recorded the fewest business closures, with just over 126,000, compared to quarter one, which saw more than 167,000. This highlights the importance of businesses having a clear growth plan in place to ensure a strong financial start to the year .

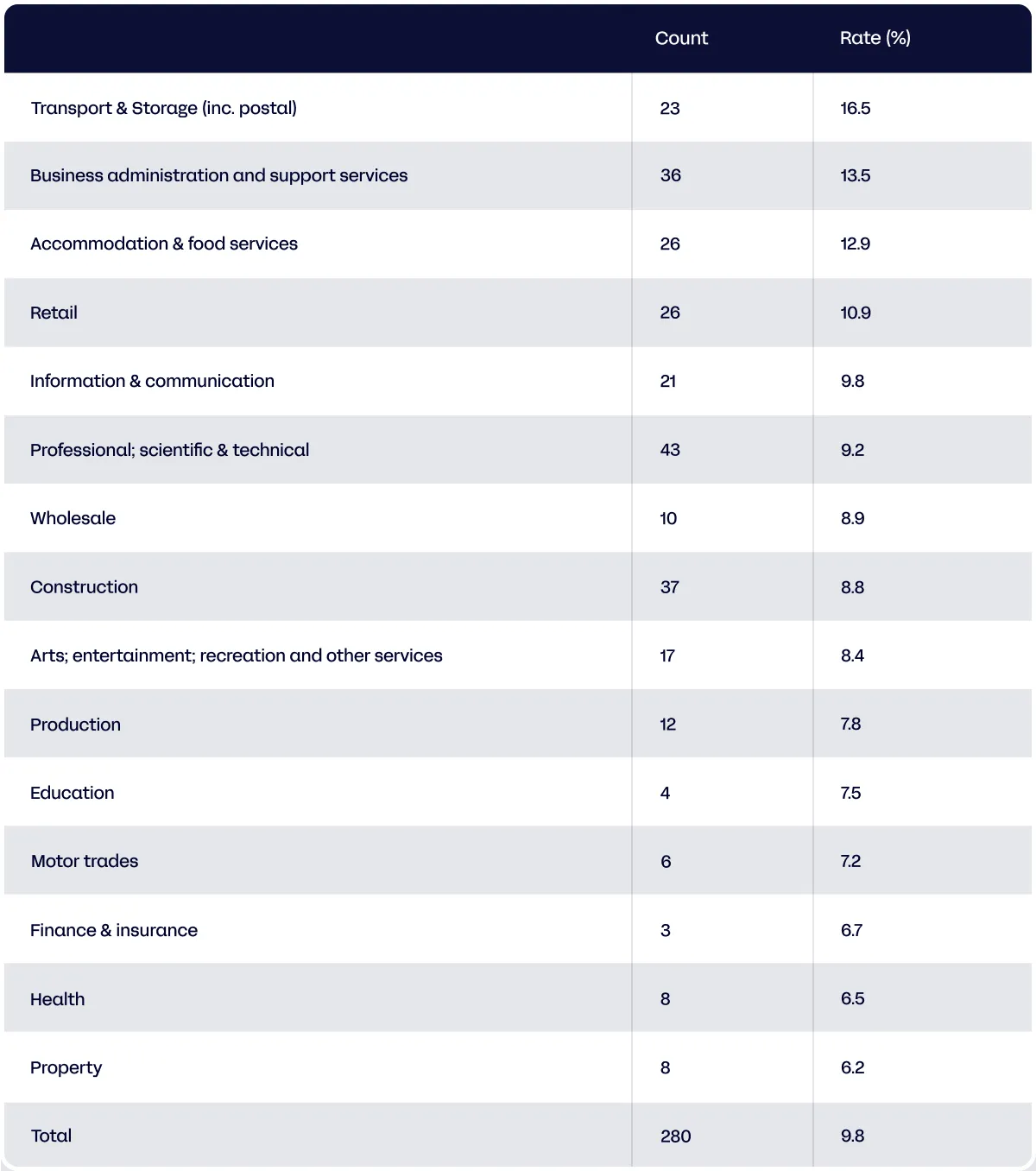

Transport and storage companies see the highest closure rate by industry group.

The latest figures highlight the percentage rate of sector-based business closures across the UK. The transport and storage sector recorded the highest rate, with 16.5% of businesses closing, resulting in around 23,000 closures compared to those remaining active.

Next was the business administration and support services sector, with a closure rate of 13.5%. Although the total number of businesses in this sector was significantly higher, at around 36,000 closures, this figure is balanced by the overall size of the sector. Following this, the accommodation and food services industry saw a closure rate of 12.9%, with many restaurants and takeaways across the UK feeling the pinch.

*Counts given to the nearest thousand

Across the table, the professional, scientific and technical sector recorded the highest number of closures, with around 43,000. The finance sector, by contrast, saw relatively low figures, with only 3,000 closures.

The property sector recorded the highest percentage rate for business survival. Despite rising demand for mortgages and increasing costs in the area, this industry remains the most resilient in terms of business continuity.

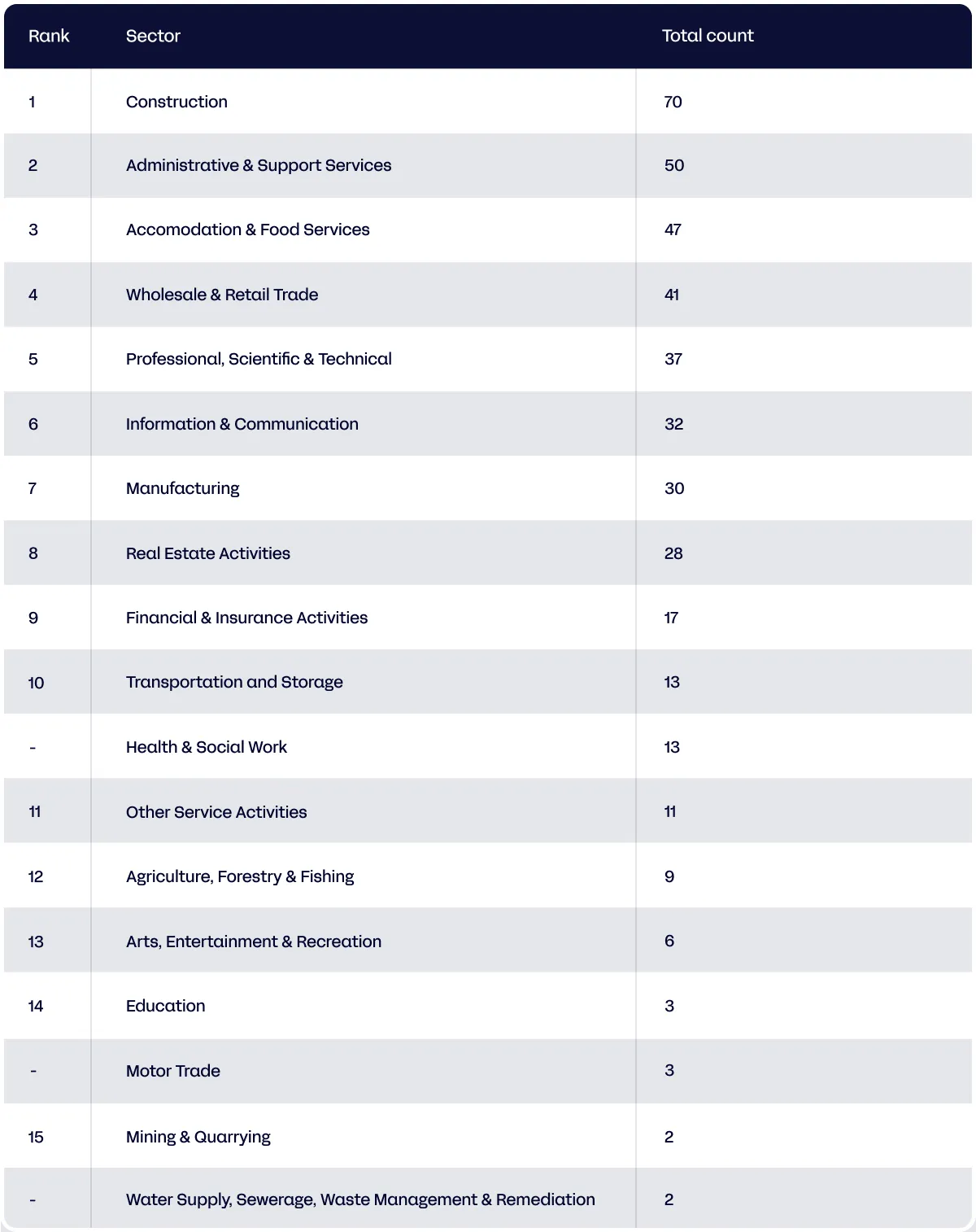

The construction sector has seen the most companies enter into liquidation.

Over the last three years, Aurum Solutions has obtained reports from Companies House showing that 432 UK companies have entered into liquidation, receivership, or administration.

Of these companies, 16% were in the construction sector. The construction sector is one of the main industries across the UK, contributing approximately £138 billion to £215.7 billion in economic value (around 6% - 7% of GDP) annually. Given the sector’s significant scale, it is perhaps unsurprising that around 70 businesses have sought financial assistance over the past few years, facing challenges such as rising costs and increased competition.

Having ranked second in terms of business closure rates, the Administrative & Support Services sector also ranks second for the number of companies entering liquidation. Over the past three years, around 50 businesses were listed, highlighting that closures are impacting this sector as well. With the rise of AI and a growing focus on efficiency, roles within this sector could face further decline.

Again, similar to the above, in third with 47 is the Accommodation & Food Service industry. The UK food system currently employs 4.1 million people, with one in eight of all UK jobs said to be in the food and drink industry. However, with intense competition among both chain and local businesses, coupled with rising food production costs and rent, the industry has faced significant pressures in recent years.

What can businesses do to help ease financial trouble?

Although data shows that many businesses are struggling and closing, the other side of the scale is that new businesses continue to launch across the UK, with the rate of new ventures steadily increasing, now at 11.1%. Whether you are a new startup seeking guidance or the owner of a long-established company looking to safeguard your operations, there are several key strategies to consider before your business finds itself in financial difficulty.

1. Prioritise cashflow visibility

Many businesses run into financial difficulty because they are alerted to problems too late. When financial data is spread across different systems, accounts, or parts of the business, issues such as missed payments or cash shortfalls are often only identified after they've caused consequences. To improve visibility, introduce weekly or even daily cash tracking. Implementing automation tools, such as Aurum’s, can help you do this without adding hours of work to your team's plate. This gives you a clearer view of money coming in and going out, upcoming costs, and overdue invoices. With a reliable, up-to-date view, you can make faster decisions, avoid unnecessary borrowing, and act early before cash pressure builds.

2. Stress test costs and evaluate commitments

While external pressures such as inflation, energy prices, and political instability add strain, risk is also increased by internal expenses where you have more control. Breaking costs into fixed, flexible, and non-essential categories makes it easier to see where you can act. From there, model simple scenarios, such as a 10 per cent drop in revenue or a rise in key costs, to understand how your margins would hold up. With the clear cash visibility established above, you can spot unnecessary spending early and make proactive changes. For example, reviewing supplier terms, logistics agreements, or unused software can reveal savings opportunities. Acting before contract renewals helps reduce pressure and protect your business as external conditions change.

3. Set internal rules

Even with clear visibility and strong planning, inconsistency across teams can still create risk. Setting simple, consistent processes across the business builds accountability and reduces avoidable errors. For smaller firms, this might mean invoicing within a set number of days after delivery, followed by regular reminders and consistent follow-up on overdue payments. For larger organisations, it often means aligning how different teams or locations handle payments and approvals. Regardless of industry or size, clear and repeatable habits improve control, reduce surprises, and help maintain a steady cash position, which is critical in avoiding closure during periods of economic uncertainty.

As market conditions continue to fluctuate, impacting the growth and potential closure of many businesses, others continue to thrive. The difference often comes down to how well organisations understand and manage their financial operations, with closures frequently prompted by financial inconsistencies.

Aurum provides an effective way to automate your finances, delivering clearer visibility, stronger controls, and greater confidence in every transaction. Explore how smarter reconciliation can strengthen your operations and protect your business’s financial future.

Methodology

Data was taken from the latest ONS business discovery data for regions that are suffering the most closures, as well as ordering the death rates of UK companies by the highest percentage rate. For the sector going into administration, data was taken from Companies House. Categories selected were liquidation, receivership, or administration, and the dissolved date was taken from the last three years.

As Aurum Solution’s CMO, Vasco Vaz Rodrigues heads up the marketing department and oversees the generation of original insights for financial professionals. Paired with Aurum’s ability to optimise their time, marketing output therefore ensures that the Aurum Solutions brand provides more than just software but holistically empowers entire finance teams.